Protect Profits by Recovering Equipment Costs | ADI Agency

Protect Profits by Recovering Equipment Costs

The ability to accurately determine job costs is fundamental to financial success for contractors. As a dealer, one of the best ways you can support your customers (and attract new ones), is to provide tips and deeper information to help them build their business. With that in mind, let’s look at the sometimes- tricky process of assigning equipment costs.

Proper job costing ensures your customers will be able to recover those costs as they bid on new projects.

The basics are pretty straight-forward

It’s easy to use your payroll system to attribute labor costs to a specific job phase code. Figures from daily time cards are assuredly accurate, and they are immediately available. Likewise, vendor charges for materials can be accurately captured from your accounts payable system. So far, so good.

However, equipment costs are more complex

Buying, maintaining, and/or renting equipment is a major expense for any contractor or other heavy equipment user. These costs must also be assigned accurately to each job – when bidding, to ensure the bid is high enough to produce a profit, and after the job is completed, to assess true profitability. Unfortunately, it’s not so easy to parcel out the costs of owning and operating equipment.

Buying, maintaining, and/or renting equipment is a major expense for any contractor or other heavy equipment user. These costs must also be assigned accurately to each job – when bidding, to ensure the bid is high enough to produce a profit, and after the job is completed, to assess true profitability. Unfortunately, it’s not so easy to parcel out the costs of owning and operating equipment.

Over time, you can calculate actual costs associated with each piece of equipment and then determine an average cost per day, week, etc. But you need those numbers upfront. One way to address that is by using predicted machine-related expenses to define a cost-recovery rate you can use consistently. That requires a calculator process or series of formulas. Exactly what works best for one company may be different for another, but the key to cost- recovery success is following the same process uniformly.

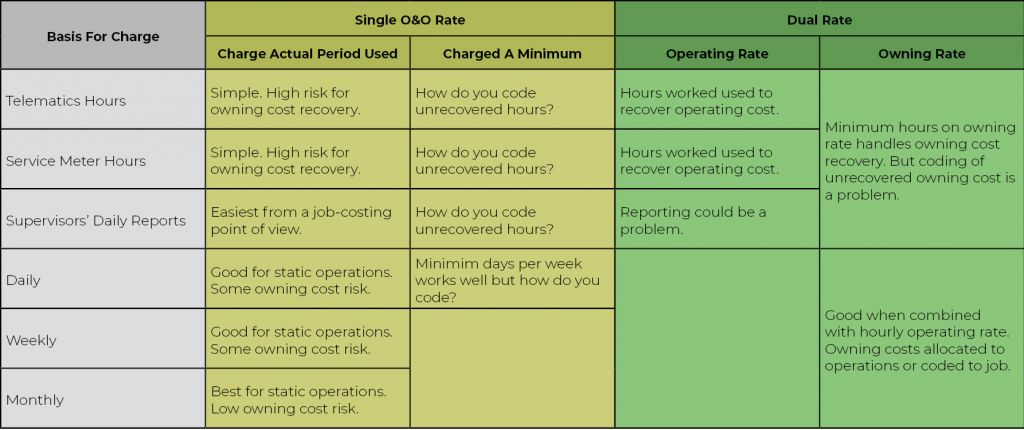

First, determine your cost-recovery basis

You can charge off equipment costs based on hours, as shown in:

- Telematics reports. This data is automatically collected and accurate, but not all machines have integrated telematics. Furthermore, some technology does not include short shutdown periods or idling time as “hours worked,” which skews the numbers.

- Service meter hours. Typically, this data must be gathered and written down by hand, a process that is both time-consuming and wide open to human error. On the other hand, someone has to collect this information anyway, as part of the overall preventive maintenance program.

- The supervisor’s daily reports. How reliable this option is depends on whether the reports are generated by hand, using honest information, or the data is collected electronically.

Instead of using hours as your basis, you could choose to use time onsite, calculating the cost-recovery rate daily, weekly, or monthly. This can be especially useful for equipment that must be available at hand but which aren’t used consistently – things such as utility tools, pumps, and message boards.

Next, determine cost-recovery rate(s)

You can lump costs of owning and operating together for each machine, or figure a rate for each expense type and charge them off separately. If you choose a single rate, you can:

- Track and charge only actual hours (or days) worked. This is simple and accurately reflects how much of a machine’s O&O costs are directly attributable to a particular job phase code. However, this doesn’t account for the general costs of owning and operating that machine as an ongoing part of the fleet, nor does it account for standing or idle time when the equipment isn’t being “used.”

- Alternatively, you can assign the cost of a pre-determined minimum number of hours (or days). This can more accurately reflect the cost of idle or standing time, also assuring that the machine is earning some money while it is onsite and unavailable to support another job. This is a plus for equipment/fleet managers, but it is sometimes viewed as a negative by site managers because their job is paying for time equipment isn’t actually working.

By charging separate rates for ownership and operation, you can address the variability of ownership costs and still calculate the fixed operating cost for the machine. This can produce more accurate cost recovery, but it also harder to implement.

One method is to charge an hourly rate to recoup operating costs plus a combination of monthly minimum and hourly rates to recoup ownership costs. In cases where hours worked are below the minimum, you can use a separate job phase standby code, using this formula below to calculate the amount:

Standby time (minimum hours – actual hours worked) X ownership rate

This also helps show how much time is being spent (i.e., wasted) with equipment standing by instead of producing work.

Another method for calculating separate O&O rates uses hours worked multiplied by hourly operating rate, but it also adds a fixed amount for daily, weekly, or monthly owning costs, based on how much time the machine is onsite. Typically, in this scenario operating costs are charged to job phase codes, whereas fixed ownership costs can be assigned to phase codes or to a separate phase code that captures all onsite equipment ownership costs.

This type of cost recovery accounting can be useful for large support equipment (tower cranes, for example) that remain onsite and are used to support multiple activities during a specific time period.

Vary the formula to the equipment

Different ways of calculating recovery costs work better for different types of equipment, and every contractor has their own preferred way of doing things. So the best advice your dealership can pass along is to “do it your way, but keep it as simple and honest as possible.” Understanding the cost recovery options and how to apply them is a great starting point.